Easy Simplest US Bank Drops for 2026

The following list details financial institutions I have personally verified through successful account openings. Note that it is recommended to decline debit card issuance, as banks typically attempt delivery to the fully associated address, prompting account closure upon discovery by the legitimate holder.

1. SunTrust Checking:

The most straightforward option: SunTrust Checking.

Ensure comprehensive details of the intended fullz (accessing a credit report enhances success). Upon accurate data entry, you will answer basic credit-related queries. Once completed, the account is active. Zelle access becomes available after 90 days.

2. Citibank Free Checking:

A driver’s licence from the corresponding state suffices (verified repeatedly). Avoid overused fullz.

After responding to standard questions, select ‘check funding’ to enable immediate online access. Zelle enrolment is permitted straightaway.

3. Discover Checking and Savings:

Provided the fullz remains unflagged, this account opens instantly with full digital access. Neither identification nor additional verification is necessary.

4. Capital One 360 Checking:

Only front and back copies of a driver’s licence are required. No security questions. Submission of an unused ID ensures immediate approval; otherwise, processing may take several days.

5. American Express Personal Savings:

No identification or verification checks are imposed. A valid fullz guarantees real-time account activation and online accessibility.

In forthcoming tutorials, I will provide illustrated walkthroughs for select account openings

Simplest US Bank Drops for 2026

Bank drops (also called “drop accounts”, “mule accounts”, or simply “drops”) are bank accounts deliberately used or controlled by criminals to receive, temporarily hold, and quickly move illegally obtained money as part of money laundering or cash-out schemes in cybercrime and financial fraud.

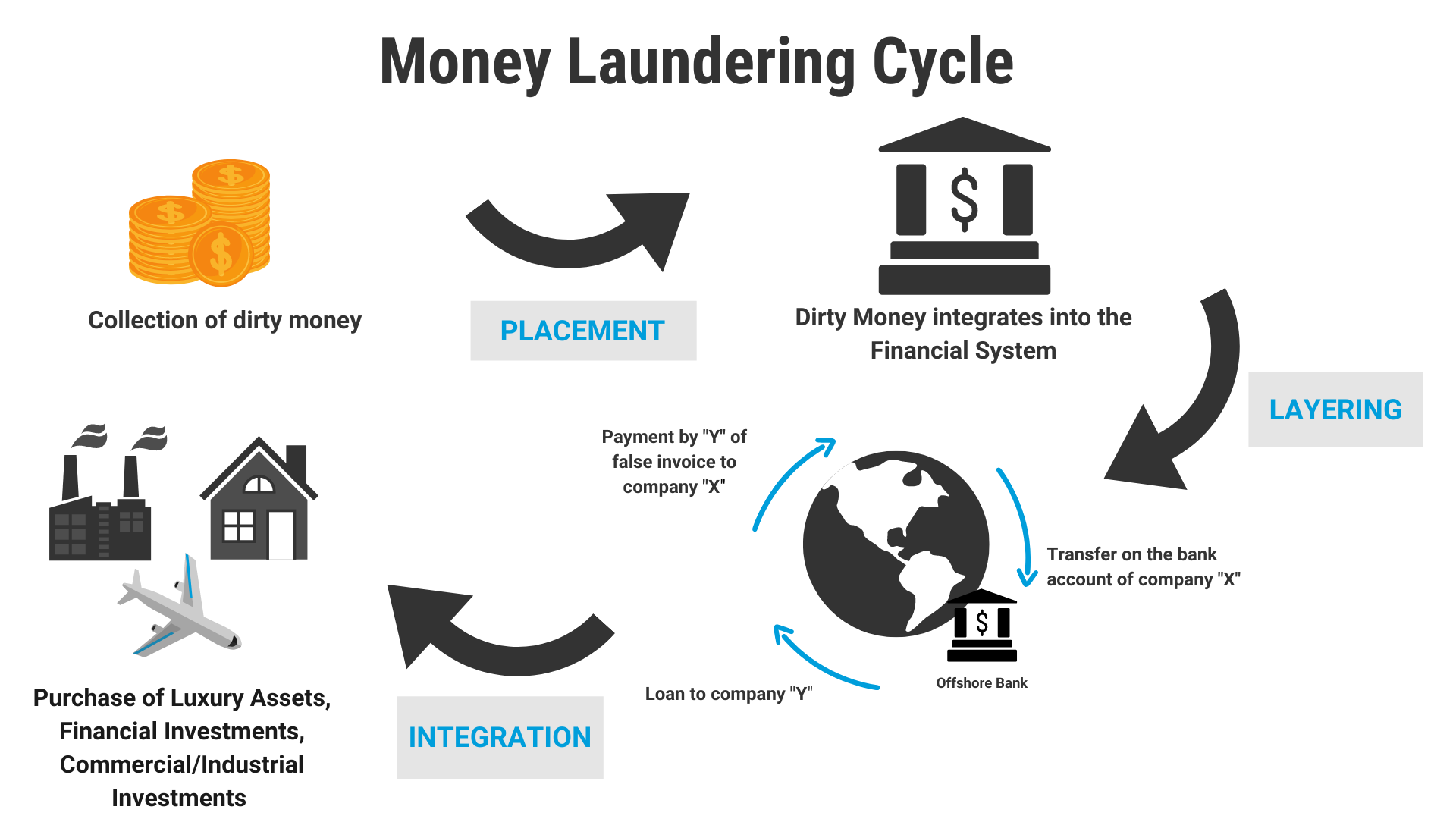

In essence, a bank drop serves as an intermediary layer in the criminal financial pipeline. Criminals obtain funds through various illegal methods—such as phishing, business email compromise (BEC), ransomware payments, card-not-present fraud, account takeovers, romance scams, investment fraud, payroll diversion, or dark-web carding—and need to distance themselves from the dirty money while converting it into usable, seemingly legitimate assets.

The core idea is simple yet effective for obscuring the trail:

-

Acquisition or creation of the account Fraudsters either:

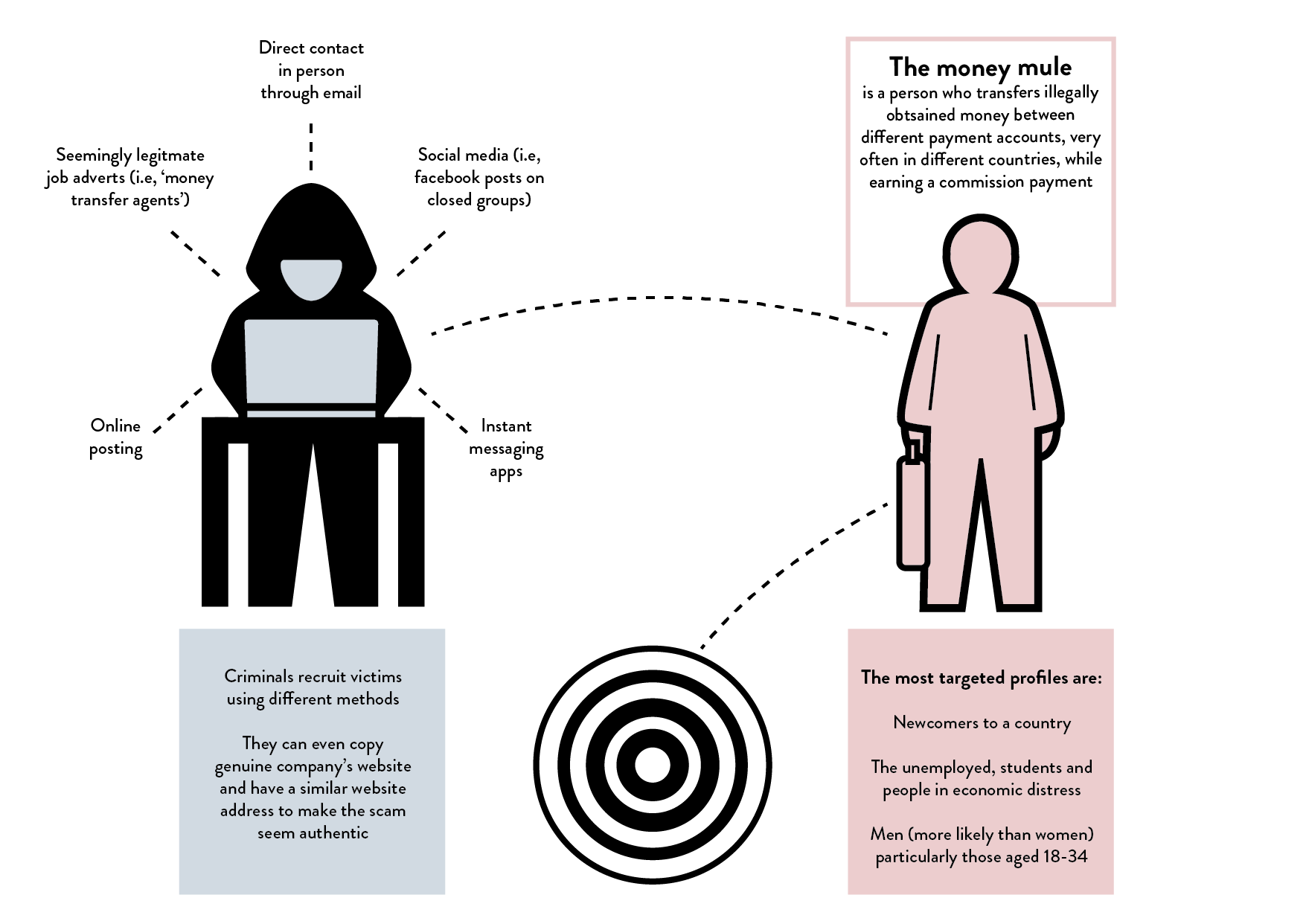

- Recruit a money mule (witting or unwitting person) who opens or hands over control of their real account in exchange for a small commission (often 5–15%).

- Use stolen or synthetic identities (“”fullz”—full personal info packages including name, SSN/ITIN, DOB, address, mother’s maiden name, etc.) to open new accounts remotely.

- Exploit compromised legitimate accounts via credential stuffing, phishing, or malware.

In 2026, fully remote openings remain possible at some online banks/fintechs (Chime, Varo, Current, Cash App, etc.), but most now demand strong KYC: government-issued photo ID, live selfie liveness check, address proof, device fingerprinting, and behavioural biometrics.

-

Placement phase The illicit funds are deposited into the drop account. Common entry points include:

- ACH/wire transfers from victim accounts are common entry points.

- Zelle/Venmo/PayPal/Cash App pushes from compromised or scammed victims.

- Check fraud deposits (fake or stolen cheques).

- Crypto-to-fiat on-ramps involve the purchase of USDT/USDC, followed by an off-ramp to the drop.

- Payroll diversion or gift card cash deposit schemes are commonly employed.

The amount is usually kept modest per transaction to avoid immediate flags (often under $3,000–$10,000 depending on the bank).

-

Layering/obfuscation phase Once inside the drop, money is moved rapidly—usually within hours or 1–2 days— to break the direct link:

- Instant transfers to other drops or mule accounts (layering chain).

- Purchases of cryptocurrency on exchanges with weak KYC.

- Gift cards are loaded or money orders are purchased.

- ATM cash withdrawals frequently involve the use of recruited mules.

- Payments are made to front entities such as fake invoices and shell companies.

The goal: create multiple hops so blockchain analysis, transaction graphing, and Suspicious Activity Reports (SARs) become harder to connect back to the original crime.

-

Integration phase Cleaned funds re-enter the economy — criminals withdraw cash, pay accomplices, invest in assets, or fund further crimes. The drop account is often abandoned or “burned” after one or two cycles.

Types of bank drops

- Witting mules — Knowingly participate for profit (common in Eastern Europe, West Africa, Southeast Asia recruitment rings).

- Unwitting mules — Tricked via fake job offers (“payment processor,” “mystery shopper”), romance scams, or overpayment schemes.

- Synthetic or stolen identity drops, which are created using fullz, pose the highest risk of rapid detection in 2026.

- Aged drops—accounts deliberately kept lowactivity for months to appear legitimate before heavy use.

Simplest US Bank Drops for 2026

Why bank drops remain popular in 2026 despite better defenses

- Real-time rails (FedNow, RTP, Zelle) allow ultra-fast movement.

- Crypto on/off-ramps provide exit liquidity.

- Global mule recruitment via Telegram, Discord, dark-web forums is still effective.

- Some fintechs still have onboarding gaps (especially for non-SSN/ITIN users or certain demographics).

Modern detection & risks (2026 reality)

Banks and fintechs now deploy:

- AI behavioral profiling (login patterns, typing speed, mouse movements).

- Device + IP + geolocation consistency checks are also implemented.

- Real-time transaction velocity rules.

- Network-wide sharing via FinCEN 314(b), LexisNexis, and Early Warning Services.

- Patterns such as rapid in/out flows on new accounts require mandatory SAR filing.

Most drops survive only days or weeks before freeze/SAR/law enforcement knock. Mules face serious charges (money laundering, conspiracy, bank fraud — up to 20+ years federal prison even if “unwitting” but reckless).

Visual examples of the concept:

This diagram illustrates the classic money laundering cycle (placement → layering → integration) where bank drops primarily sit in the placement and layering stages.

Simplest US Bank Drops for 2026

Recruitment tactics targeting vulnerable people (students, unemployed, newcomers) to become unwitting mules.

Simplest US Bank Drops for 2026

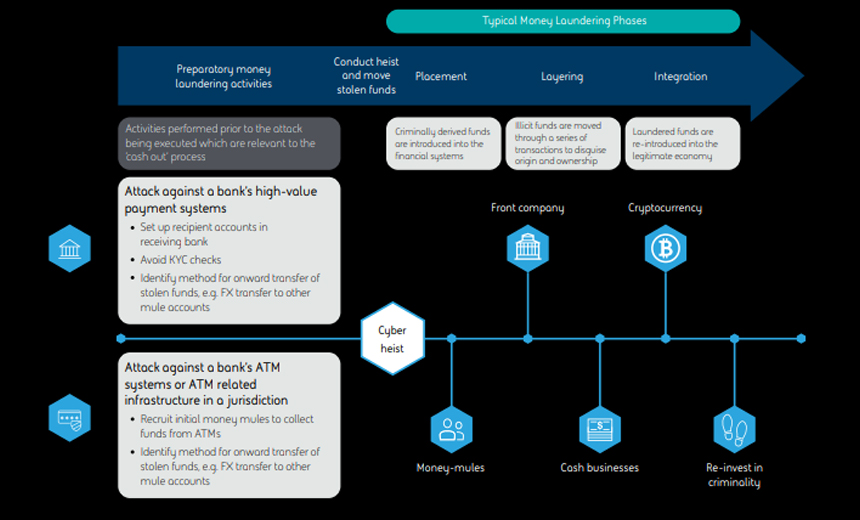

This article provides a high-level view of how cybercriminals structure their attacks to feed funds into drop networks.

In summary, bank drops are disposable or controlled accounts that form the backbone of modern financial cybercrime cash-out infrastructure. They exploit gaps in onboarding, human greed/naivety, and speed of digital money movement — but face increasingly hostile defences. Engaging in or facilitating them carries extreme legal risk.

Simplest US Bank Drops for 2026

Banks/Fintechs That Scammers Have Historically Targeted (But Are Now High-Risk / Difficult in 2026)

These appear in fraud forums as “easiest” targets, but success rates have dropped sharply:

- Chime — Still frequently mentioned for fast signup (SSN required, but some try synthetic IDs). Very aggressive early fraud holds/freezes on new accounts.

- Cash App (Block) — Easy mobile signup, Bitcoin support. Heavily monitored; limits hit fast, accounts closed quickly on suspicious patterns.

- Varo Bank — Online-only, no-fee checking. Requires SSN/ITIN; strong early-transaction monitoring.

- Current or Green Dot reloadable accounts — Sometimes used via prepaid routes. Very low limits and fast shutdowns.

- Major online banks like Ally, SoFi, Capital One 360 — Require full KYC; excellent fraud teams; almost impossible for clean drops.

- Revolut or Wise (multi-currency) — Some non-residents try for USD accounts, but strict verification and very low tolerance for fraud.

Why “Simplest” Drops Are No Longer Simple in 2026

- Most legitimate US banks/fintechs now require SSN/ITIN + government-issued photo ID + address proof (utility bill, lease) for interest-bearing or full-featured accounts.

- Non-SSN options (ITIN or passport-only) exist mainly for legal non-residents/immigrants at select banks (Bank of America, Chase, PNC, some credit unions like Self-Help), but they still demand strong verification and flag unusual activity instantly.

- Synthetic/fake identities get detected via LexisNexis, device fingerprinting, behavioral biometrics, and cross-bank data sharing.

- Cashout paths (Zelle, Venmo, crypto on-ramps) are heavily restricted or frozen on new/high-risk accounts.

Simplest US Bank Drops for 2026